The rapid growth of stablecoins–crypto-assets aimed at maintaining a stable value–has generated a sizable demand for short-term dollar-denominated assets. Stablecoin issuers hold these assets to back their tokens and manage their peg. This paper shows that an increase in the demand for stablecoin tokens caused additional commercial paper (CP) issuance, when tokens were backed by CP. This suggests CP issuers catered to the demand emanating from stablecoins’ backing. Our results highlight a new and more general link between crypto-assets, conventional financial markets, and short-term debt issuers.

@article{barthelemy2025stablecoins,title={Stablecoins and short-term funding markets},author={Barthélemy, Jean and Gardin, Paul and Nguyen, Benoit},journal={Journal of International Money and Finance},pages={103469},year={2025},doi={https://doi.org/10.1016/j.jimonfin.2025.103469},}

Revisiting the Dynamic Impact of Asset Purchases: A Survey-Based Identification

We propose a novel instrument for identifying central bank asset purchase shocks in a proxy-VAR. Our instrument exploits the deviations between asset purchase announcements and expectations inferred from quantitative surveys. Using euro area data, we find a positive impact of purchases on macroeconomic variables with high posterior probability. An asset purchase shock of 1% of GDP leads to median impacts on output and prices of 0.12% and 0.07%, respectively. The effects are three times as small as those in the US economy. Finally, we show that our instrument is stronger than high-frequency instruments, both in terms of statistical strength and alignment with narrative evidence.

@article{lhuissier2025survey,author={Lhuissier, Stéphane and Nguyen, Benoît},title={Revisiting the Dynamic Impact of Asset Purchases: A Survey-Based Identification},journal={Journal of Applied Econometrics},volume={40},number={7},pages={846-861},keywords={asset purchase programme, Eurosystem, monetary policy, proxy-VAR},doi={https://doi.org/10.1002/jae.70011},url={https://onlinelibrary.wiley.com/doi/abs/10.1002/jae.70011},eprint={https://onlinelibrary.wiley.com/doi/pdf/10.1002/jae.70011},year={2025},}

2021

Inspecting the mechanism of quantitative easing in the euro area

Ralph S.J.

Koijen, François

Koulischer, Benoît

Nguyen, and

1 more author

Using security-level holdings for all euro-area investors, we study portfolio rebalancing during the quantitative easing program from March 2015 to December 2017. Foreign investors outside the euro area accommodated most of the Eurosystem’s purchases. Duration, government credit, and corporate credit risk did not get concentrated in particular regions or investor sectors. We estimate a demand system for government bonds by instrumental variables to relate portfolio rebalancing to yield changes. Government bond yields decreased by 65 basis points on average, and this estimate varies from 38 to 83 basis points across countries.

@article{koijen2021euroarea,title={Inspecting the mechanism of quantitative easing in the euro area},journal={Journal of Financial Economics},volume={140},number={1},pages={1-20},year={2021},issn={0304-405X},doi={https://doi.org/10.1016/j.jfineco.2020.11.006},url={https://www.sciencedirect.com/science/article/pii/S0304405X20303123},author={Koijen, Ralph S.J. and Koulischer, François and Nguyen, Benoît and Yogo, Motohiro},keywords={Portfolio rebalancing, Quantitative easing, Risk concentration, Unconventional monetary policy},}

2020

The scarcity effect of QE on repo rates: Evidence from the euro area

William

Arrata, Benoît

Nguyen, Imène

Rahmouni-Rousseau, and

1 more author

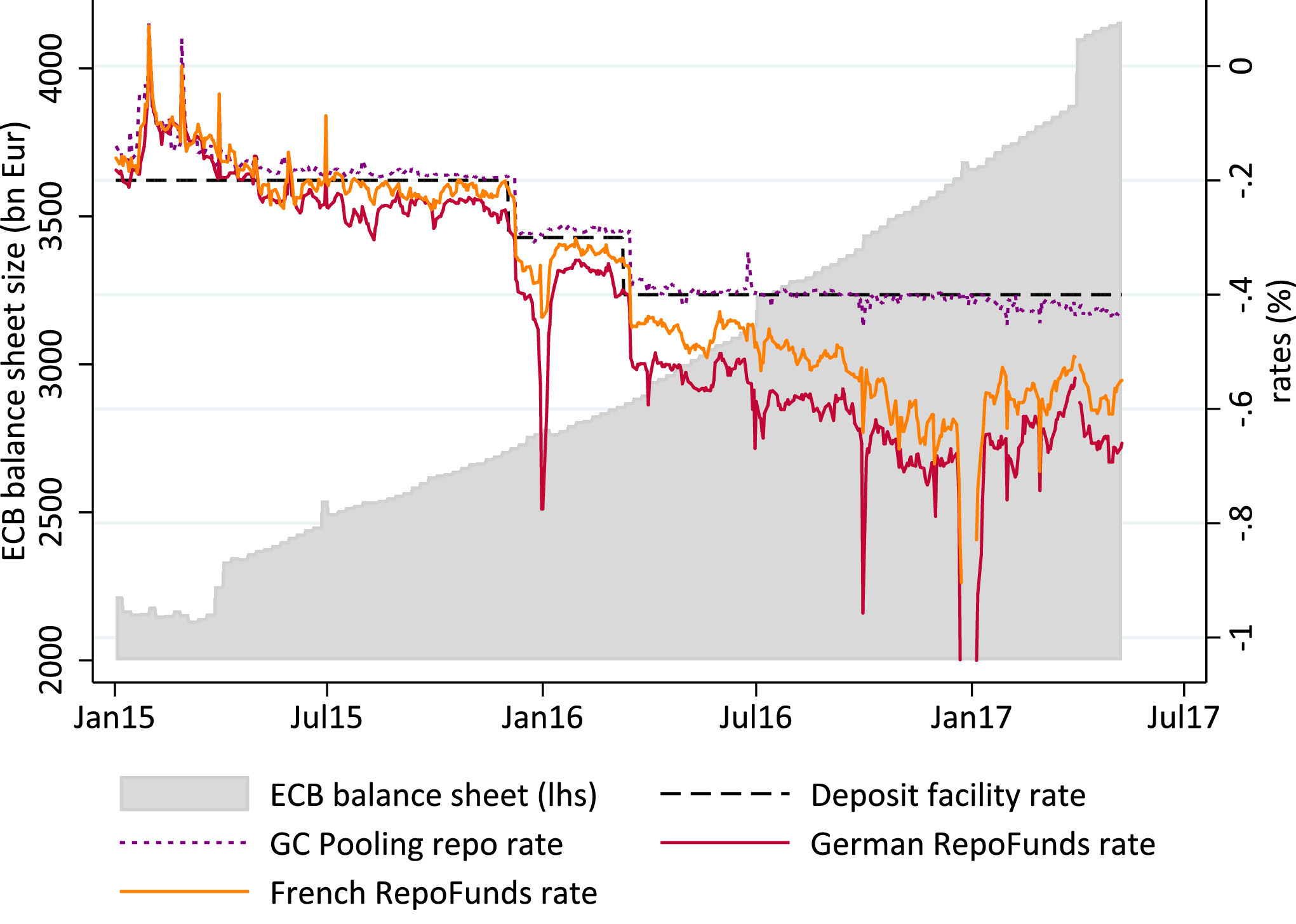

Most short-term interest rates in the euro area are below the European Central Bank deposit facility rate, the rate at which the central bank remunerates banks for excess reserves. This coincided with the start of the Public Sector Purchase Program (PSPP) launched in March 2015. In this paper, we explore empirically the interactions between the PSPP and repo rates. Using proprietary data from PSPP purchases and repo transactions for specific (“special”) securities, we assess the scarcity channel of PSPP and its impact on repo rates. We estimate that purchasing 1% of a bond outstanding is associated with a decline of its repo rate of 0.78 basis points.

@article{arrata2020scarcity,title={The scarcity effect of QE on repo rates: Evidence from the euro area},journal={Journal of Financial Economics},volume={137},number={3},pages={837-856},year={2020},issn={0304-405X},doi={https://doi.org/10.1016/j.jfineco.2020.04.009},url={https://www.sciencedirect.com/science/article/pii/S0304405X20301240},author={Arrata, William and Nguyen, Benoît and Rahmouni-Rousseau, Imène and Vari, Miklos},keywords={Specialness, Repo market, Asset purchases, Money market},}

2017

Euro-Area Quantitative Easing and Portfolio Rebalancing

Ralph S. J.

Koijen, François

Koulischer, Benoît

Nguyen, and

1 more author

American Economic Review: Papers and proceedings, May 2017

@article{10.1257/aer.p20171037,author={Koijen, Ralph S. J. and Koulischer, François and Nguyen, Benoît and Yogo, Motohiro},title={Euro-Area Quantitative Easing and Portfolio Rebalancing},journal={American Economic Review: Papers and proceedings},volume={107},number={5},year={2017},month=may,pages={621–27},doi={10.1257/aer.p20171037},url={https://www.aeaweb.org/articles?id=10.1257/aer.p20171037},}

Working Papers

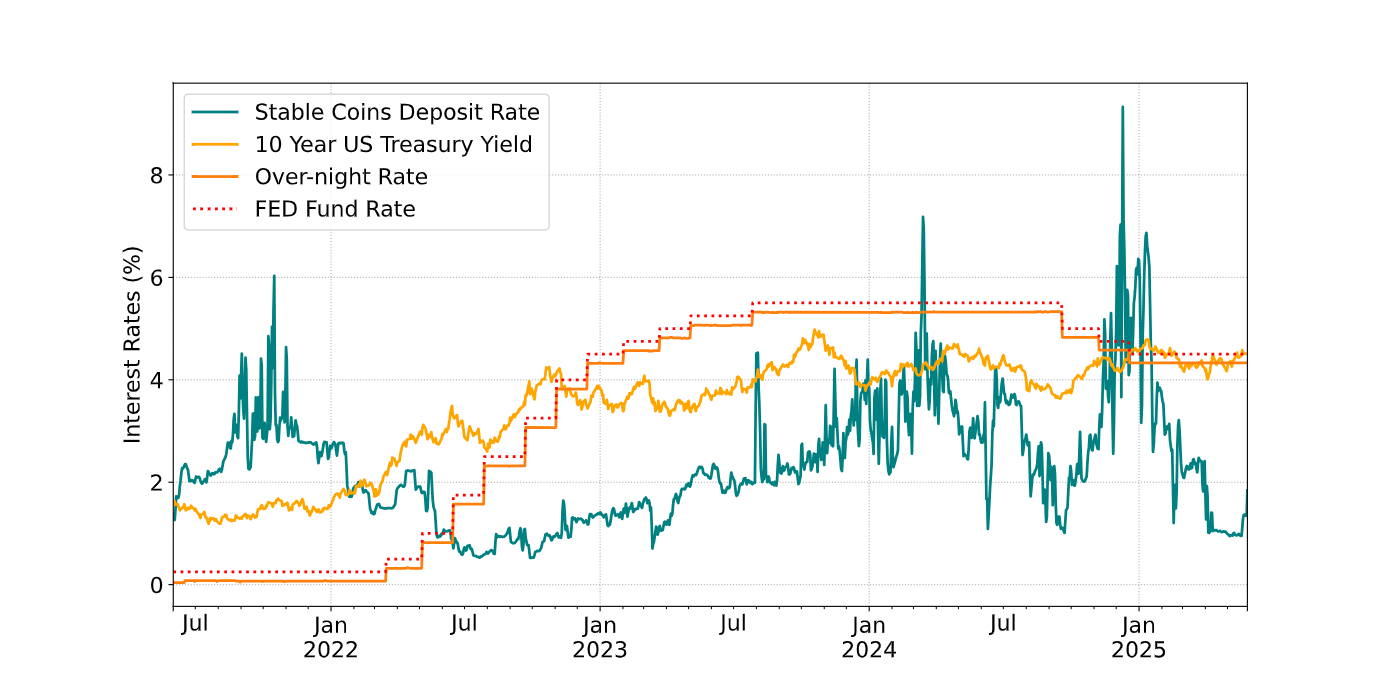

DeFi-ying the Fed? Monetary Policy Transmission to Stablecoin Rates

Does the Federal Reserve’s monetary policy influence the rates on USD-pegged stablecoins? While major stablecoin issuers do not pay interest, investors can earn returns by lending stablecoins in Decentralized Finance (DeFi) platforms. This paper documents a disconnect between conventional short-term interest rates and the deposit rate of USD-pegged stablecoins in DeFi. We develop a simple model of DeFi to rationalize this disconnect and empirically test its predictions. Our results show that after controlling for DeFi-specific factors, US monetary policy has a —limited but significant— passthrough to stablecoin lending rates, explaining only a limited fraction of their variation. This suggests excess returns in stablecoin lending markets are primarily driven by crypto-specific, demand-driven shocks and persist as stablecoin lending supply responds sluggishly. Going forward, arbitrage between traditional money market and DeFi rates may, however, be facilitated by lower frictions, lower fees, and a greater convergence enabled by real-world assets tokenization.

@unpublished{barbon2025defi,title={DeFi-ying the Fed? Monetary Policy Transmission to Stablecoin Rates},author={Barbon, Andrea and Nguyen, Benoit and Barthelemy, Jean},journal={SSRN Electronic Journal},year={2025},publisher={Elsevier BV},doi={https://dx.doi.org/10.2139/ssrn.4673325},}

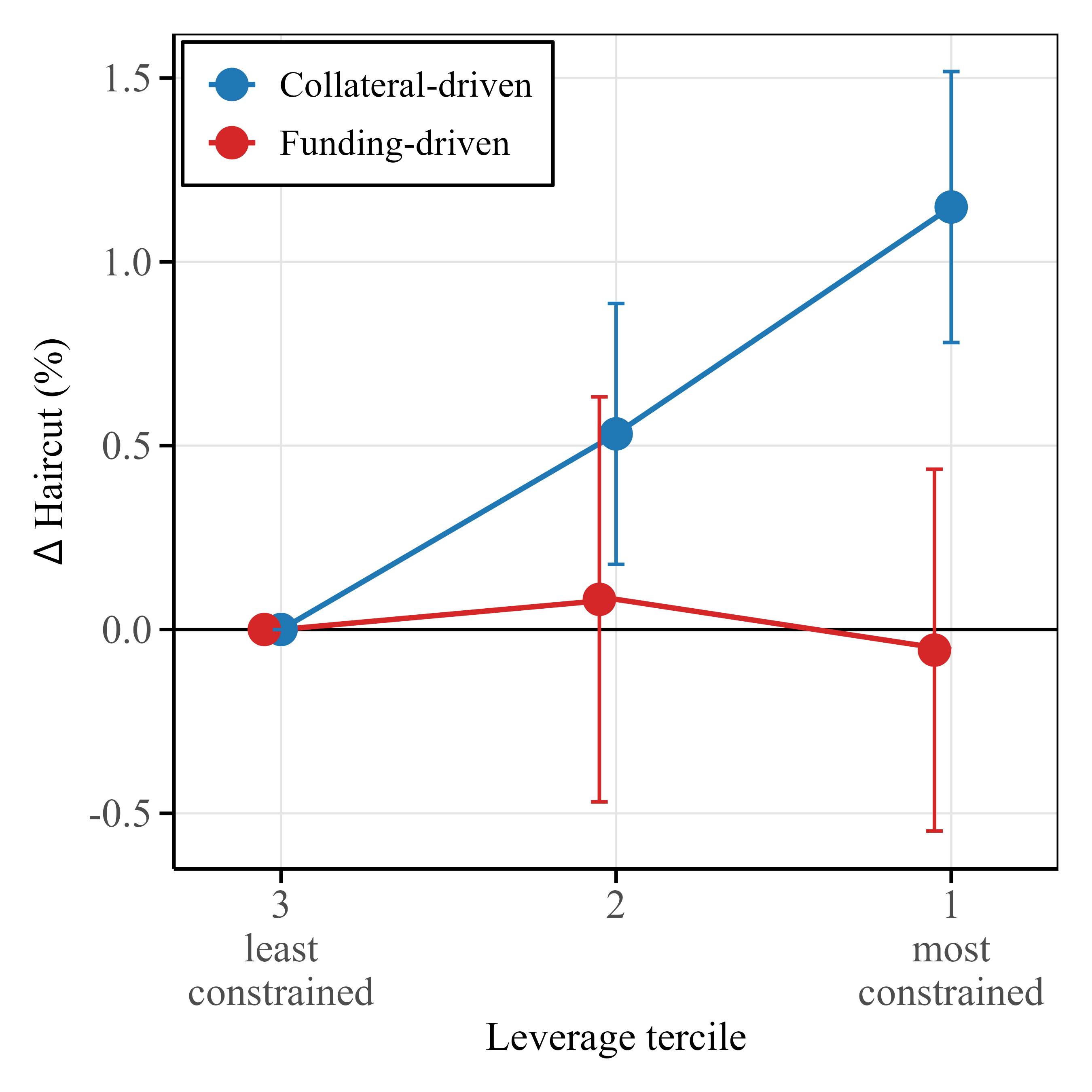

We investigate how frictions in euro area repo markets distort the setting of haircuts - often presented as the main risk management tool in repo transactions. Using unique European repo data, we show that balance sheet constraints, collateral heterogeneity, and dealer market power lead to suboptimal haircuts, especially in collateral-driven repos. We develop a theoretical model explaining these distortions and their effects on market outcomes. Our findings highlight the underlying frictions behind suboptimal haircuts which result in more volatile repo rates and volumes, and have important implications for monetary policy and financial stability.

@unpublished{Ballensiefen2025haircuts,author={Ballensiefen, Benedikt Fabian and Nguyen, Benoît and Knyphausen, Jasper},doi={10.2139/ssrn.5939177},issn={1556-5068},journal={SSRN Working Paper},title={Stop Believing in Haircuts},year={2025},}

Paying Banks to Lend? Evidence from the Eurosystem’s TLTRO and the Euro Area Credit Registry

Emilie Da

Silva, Vincent

Grossmann-Wirth, Benoît

Nguyen, and

1 more author

In response to the pandemic, the Eurosystem embedded a transfer mechanism in its lending operations to the banking system, during a “Special Interest Rate Period”. Using the newly available euro area credit registry, we study the effect of this direct transfer to banks. We exploit an exogenous change in the size of the program and find statistically significant effects on credit supply. We compare the impact of this program to other government interventions to support the banking system in times of crisis.

@unpublished{DaSilva2021sirp,author={Silva, Emilie Da and Grossmann-Wirth, Vincent and Nguyen, Benoît and Vari, Miklos},doi={10.2139/ssrn.3968921},issn={1556-5068},journal={Banque de France Working Paper WP 848},title={Paying Banks to Lend? Evidence from the Eurosystem's TLTRO and the Euro Area Credit Registry},year={2021},}